UK's productivity crisis deepens as stagnant growth leaves wages frozen for decades

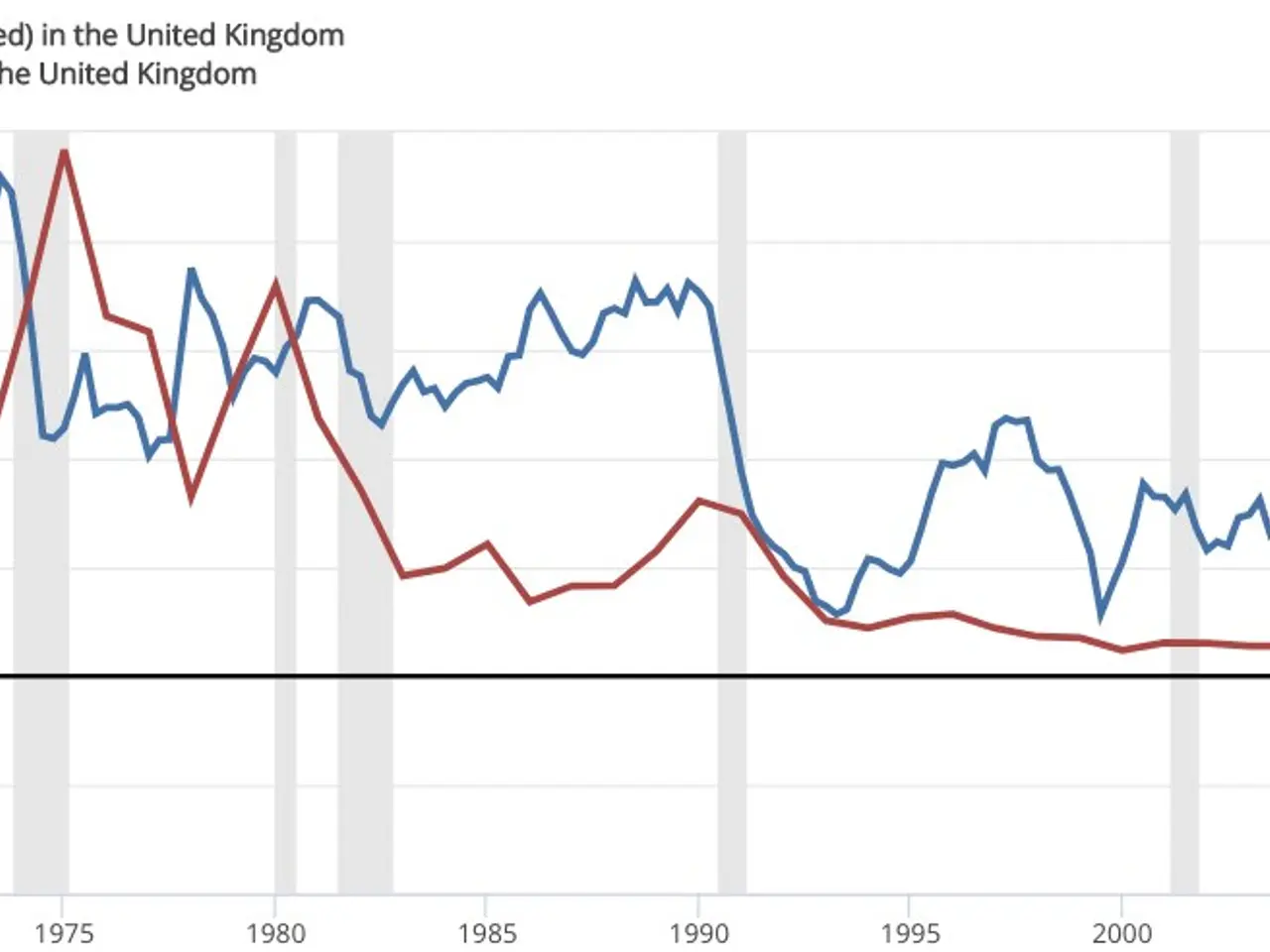

The UK faces a long-standing productivity crisis that has slowed economic growth for decades. While living standards once doubled every 28 years, progress has now stalled to the point where it could take nearly 80 years to achieve the same improvement. Experts suggest that unlocking the country’s vast household savings could help turn the tide—if people can be encouraged to invest more wisely. From the 1980s to the mid-1990s, UK labour productivity grew by 2.5% each year. This steady rise allowed Generation X to earn roughly twice as much as their parents in real terms. But since the mid-1990s, productivity growth has slumped, leaving the UK trailing behind other advanced economies. Today, British workers are 15% less productive than those in Germany, the Netherlands, and the US—and a striking 46% behind Norway.

The slowdown has left many households sitting on significant savings. Around 13.5 million UK families hold between £10,000 and £250,000 in net financial wealth, adding up to roughly £800 billion. Nationwide, Britons keep about £2.3 trillion in cash, much of which is losing value to inflation. Economists argue that redirecting even a fraction of this money into productive investments could help close the UK’s investment gap and revive growth. Yet most people remain hesitant to invest. Fear of losing money and the challenge of balancing investments with work and family life keep savings locked away. To change this, policymakers have proposed better financial education, tax incentives for investors, and new products like infrastructure bonds. Even small, regular contributions—such as £25 a month in the stock market—could, over time, help more people build wealth while supporting broader economic recovery.

The UK’s productivity gap is deep-rooted, stretching back nearly three decades. Without intervention, the slowdown risks prolonging stagnant wages and living standards. Mobilising household wealth through smarter investment could offer a path forward—but only if barriers to participation are addressed and confidence in markets is restored.

Read also:

- India's Agriculture Minister Reviews Sector Progress Amid Heavy Rains, Crop Areas Up

- Sleep Maxxing Trends and Tips: New Zealanders Seek Better Rest

- Over 1.7M in Baden-Württemberg at Poverty Risk, Emmendingen's Housing Crisis Urgent

- Life Expectancy Soars, But Youth Suicide and Substance Abuse Pose Concern

{kind=link}