Multiply, commanded by Simon Brown, proceed!

In the dynamic world of finance, the valuations in US markets have reached extreme levels, not limited to high-flying tech stocks. This phenomenon is primarily due to concentrated growth in a few key sectors, especially technology and AI-related industries, which have driven price-to-earnings (P/E) multiples significantly above historic and five-year averages.

The Nasdaq's earnings multiple is a prime example of this trend. The optimism surrounding AI-driven earnings growth and new technologies is pushing prices higher than typical earnings growth justifies, creating valuation levels comparable to or exceeding those of previous market bubbles like the dot-com era.

However, it's essential to note that the broader market trades closer to fair value. Growth stocks, particularly the largest five, have increased their fair value estimates sharply, pushing overall market multiples higher.

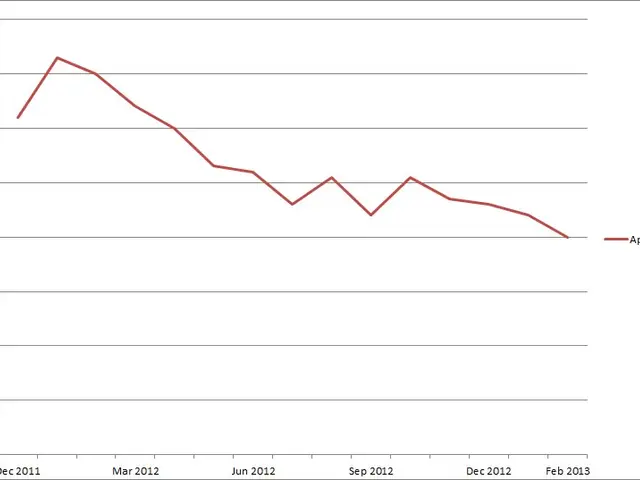

One company that stands out in this context is Costco, a membership bulk-buying warehouse business in the US. Although exact current and historic earnings multiple figures are not readily available, Costco's earnings multiple is likely lower and less volatile than the tech-driven Nasdaq average. Typically, Costco trades at a moderate P/E multiple reflecting steady earnings growth.

However, the current valuation of Costco suggests a potential overvaluation in the US market, given its deviation from its long-term average. The company's current earnings multiple is nearly double its historic average, currently sitting just under 50. This is significantly higher than the five-year average of the Nasdaq earnings multiple, which remains about 30.

Moreover, the current valuation of Costco, despite being in a different sector, still shows signs of being at extreme levels. The current valuation of Costco, while currently exceeding its five-year average, is still lower than the Nasdaq's current earnings multiple, which is in the mid-30s.

This discrepancy between Costco's valuation and the Nasdaq's valuation could indicate a potential risk for investors. Valuations in key sectors like financials and industrials may also be overestimated given expectations for slowing economic growth in 2025, calling for caution.

In conclusion, while the US market's valuations are at extreme levels, with the Nasdaq's earnings multiple being a prime example, it's crucial for investors to consider the individual company's performance and long-term average earnings multiples before making investment decisions. Costco, despite being a value-oriented company, shows signs of overvaluation, which could indicate a potential risk for investors.

Investors should be mindful of the current valuations in the US market, particularly in technology and AI-related industries, as the enthusiasm for AI-driven earnings growth is propelling prices beyond typical earnings growth justification, similar to previous market bubbles like the dot-com era. Remarkably, the current valuation of Costco, a US membership bulk-buying warehouse business, reveals signs of overvaluation, with its earnings multiple nearly doubling its historic average, currently at nearly 50. This is significantly higher than the five-year average of the Nasdaq earnings multiple, which remains around 30, indicating a potential risk for investors.

{kind=link}