Key Points for Redeeming Your Investments Priorly

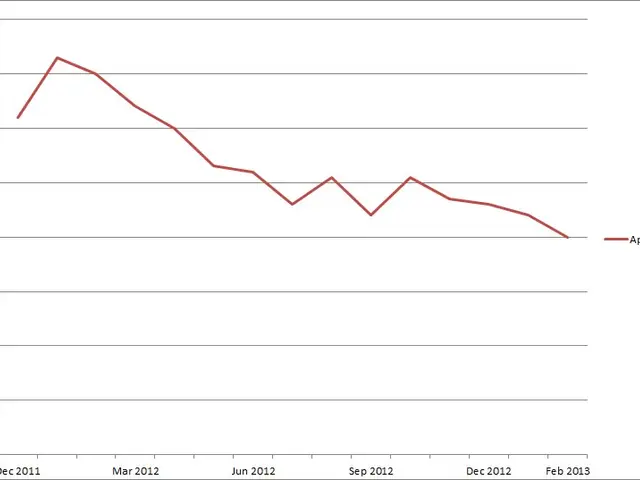

Investing in mutual funds can be a lucrative venture, as demonstrated by an investor who exited their investments in July 2011 and restarted investing from Sep 2012, earning an impressive XIRR of 14.08%. However, the value of SIP investments can fluctuate based on market movements, and premature redemption can lead to missed opportunities.

One such example is an investor who exited their investments in 2008 before the market recovered, missing out on potential gains and a potential 13% return. This underscores the importance of understanding how SIP investments work and the benefits they offer before making any decisions to exit.

It's not uncommon for the value of SIP investments to dip below the invested sums, as shown in another example between October 2008 and March 2009. However, staying invested during such periods can help investors benefit from long-term compounding and averaging effects.

Redeeming a sum and parking it in a bank account can also be detrimental. Idling balance in a bank account earns poor interest compared to what they could earn if invested in a short-term debt fund or a liquid fund. Additionally, redeeming a sum can attract tax on cumulative interest earnings over Rs 10,000.

The potential consequences of unplanned redemption in mutual funds include paying exit loads (early withdrawal fees), incurring capital gains tax, losing out on compounding growth, and facing liquidity risks or underperformance exposures. To avoid these negative consequences, investors can plan redemptions according to their financial goals, hold funds for longer than the minimum holding period to avoid exit loads and benefit from lower long-term capital gains tax rates, use portfolio rebalancing strategically, apply tax-loss harvesting, and consider pledging mutual fund units as collateral to unlock liquidity without needing to redeem and sell investments.

In summary, the key to avoiding the drawbacks of unplanned redemption is disciplined, goal-oriented planning, understanding the tax and fee structures, and leveraging alternatives to outright redemption for liquidity needs. This approach helps minimize costs, taxes, and lost growth opportunities while maintaining portfolio alignment with investor objectives.

It's also crucial to resist the urge to panic during periods of sustained loss. Panicking can lead to missed opportunities, as shown in the examples provided. If there is no clear reason to make a redemption, it is best to stay invested until there is a clear sign on why to exit the investment.

In the end, investing in mutual funds for the long term, particularly through a Systematic Investment Plan (SIP), can be beneficial due to the averaging and compounding effects. Short-term capital gains can be worked around to reduce tax implications, but it's always best to consult with a financial advisor before making any decisions.

- Instead of exiting mutual funds prematurely, like the investor who missed out on a potential 13% return in 2008, it's essential to understand the benefits of SIP investments and their potential for long-term growth.

- During market downturns, such as the period between October 2008 and March 2009, staying invested in mutual funds can lead to greater returns due to the compounding and averaging effects.

- Investors can avoid the drawbacks of unplanned redemption in mutual funds by having a disciplined, goal-oriented investment plan, understanding the tax and fee structures, and utilizing strategies like portfolio rebalancing, tax-loss harvesting, and pledging mutual fund units as collateral to unlock liquidity.

{kind=link}